Written by

Christopher Callaghan

Published on

July 14, 2025

An iMARCK Resources Analysis of Global Market Forces, Investor Behavior, and Economic Drivers

At iMARCK Resources, we operate at the center of the global gold market—connecting producers, investors, governments, and downstream users across continents. Understanding what drives the price of gold is essential not only for trading and investment but also for policy planning, mine development, and long-term economic forecasting. While gold is often considered a “safe haven,” its price is shaped by a complex and dynamic interplay of global forces, both macroeconomic and geopolitical. This white paper examines the major factors that influence the price of gold, offering insights that guide our global strategies and partnerships in gold exploration, trading, and investment facilitation.

Gold differs from other commodities in one critical respect: it is not consumed in the traditional sense. While some gold is used in electronics and jewelry, the vast majority is held in reserve—either by central banks, institutional investors, or private holders. As such, gold's value is not driven solely by supply and demand for physical use, but by investor sentiment, monetary policy, currency fluctuations, and global risk perceptions.

One of the most significant drivers of gold prices is macroeconomic uncertainty. In periods of inflation, recession, currency devaluation, or financial market instability, investors often turn to gold as a store of value. This “flight to safety” behavior increases demand and, subsequently, price. For instance, during the 2008 financial crisis and the COVID-19 pandemic, gold prices surged as equity markets faltered and central banks injected liquidity into the system. Historically, whenever trust in fiat currencies diminishes, gold has been viewed as a hedge against systemic risk.

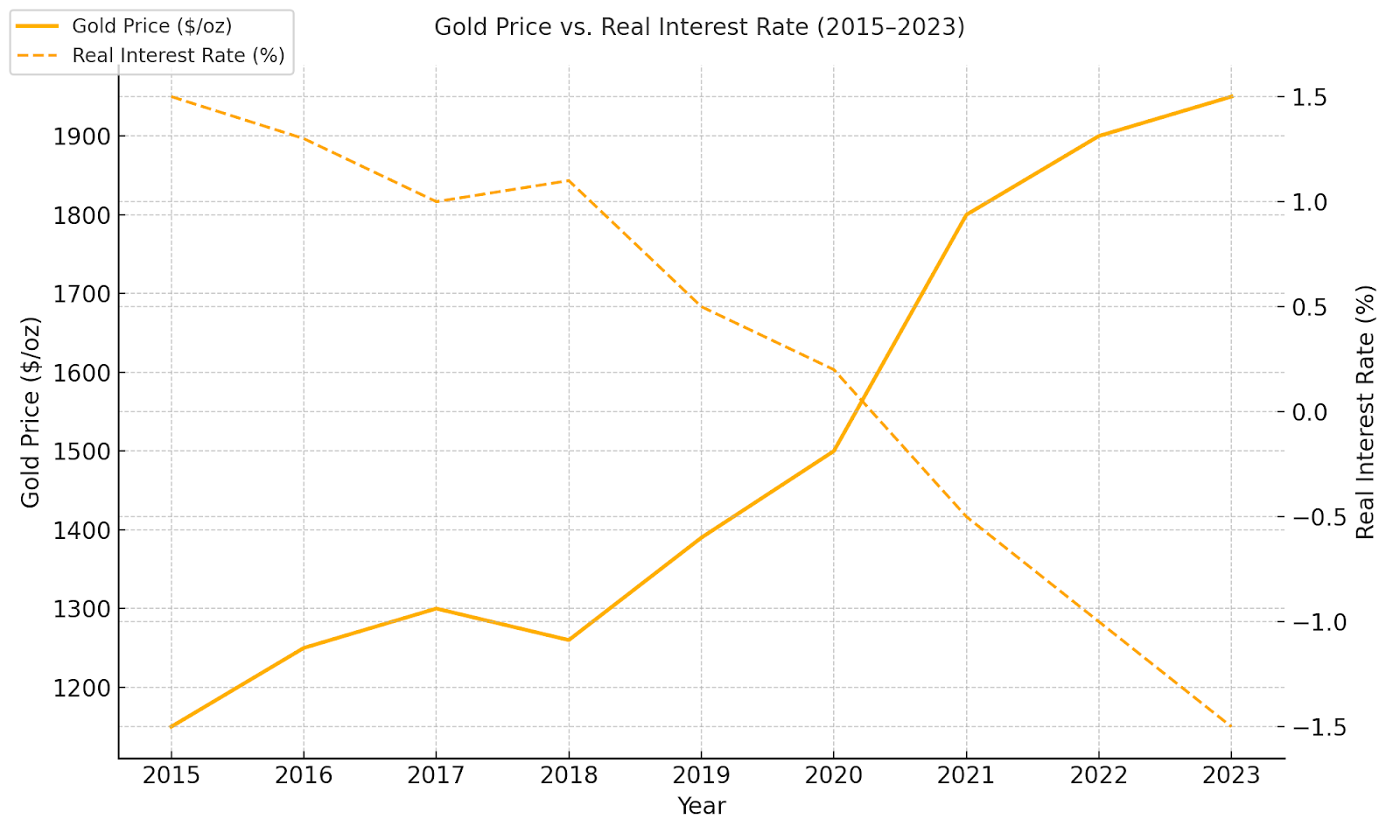

Interest rates, particularly U.S. real interest rates (the rate after inflation), also have a strong inverse relationship with gold prices. When real interest rates are low or negative, the opportunity cost of holding non-yielding assets like gold diminishes, making it more attractive to investors. Conversely, when rates rise, especially if they outpace inflation, gold may become less appealing relative to interest-bearing assets like bonds. As a result, central bank policies—especially those of the U.S. Federal Reserve—play an outsized role in shaping market expectations for gold prices.

Figure 1: Gold prices tend to move inversely with real interest rates. Lower real yields increase the attractiveness of holding gold.

Closely tied to interest rates is the strength or weakness of the U.S. dollar, which has a typically inverse relationship with gold. Because gold is priced in dollars, a stronger dollar makes gold more expensive for foreign investors, dampening demand. When the dollar weakens, gold becomes relatively cheaper in local currencies, thus increasing global demand. Therefore, fluctuations in currency markets—including geopolitical shifts, trade balances, and international sanctions—can all influence gold pricing dynamics.

Inflation expectations are another key variable. While gold is often touted as an inflation hedge, it is more accurately a hedge against unanticipated inflation or long-term structural inflation. If investors believe inflation will rise persistently—without sufficient policy response—they tend to increase gold holdings. However, in periods of low, stable inflation or deflation, gold may lose favor to yield-generating assets. In this context, gold’s role as a “monetary metal” becomes more prominent than its role as a raw material.

On the supply side, global mine production and recycling activity do influence long-term price trends, although they tend to have a more gradual impact. Gold mining is capital-intensive, highly regulated, and environmentally sensitive. Disruptions in politically unstable regions, rising energy costs, labor shortages, and ESG compliance requirements can constrain supply and create upward price pressure. At iMARCK Resources, we closely monitor these factors, especially in emerging markets where we support mining development through public-private partnerships and investor pairing.

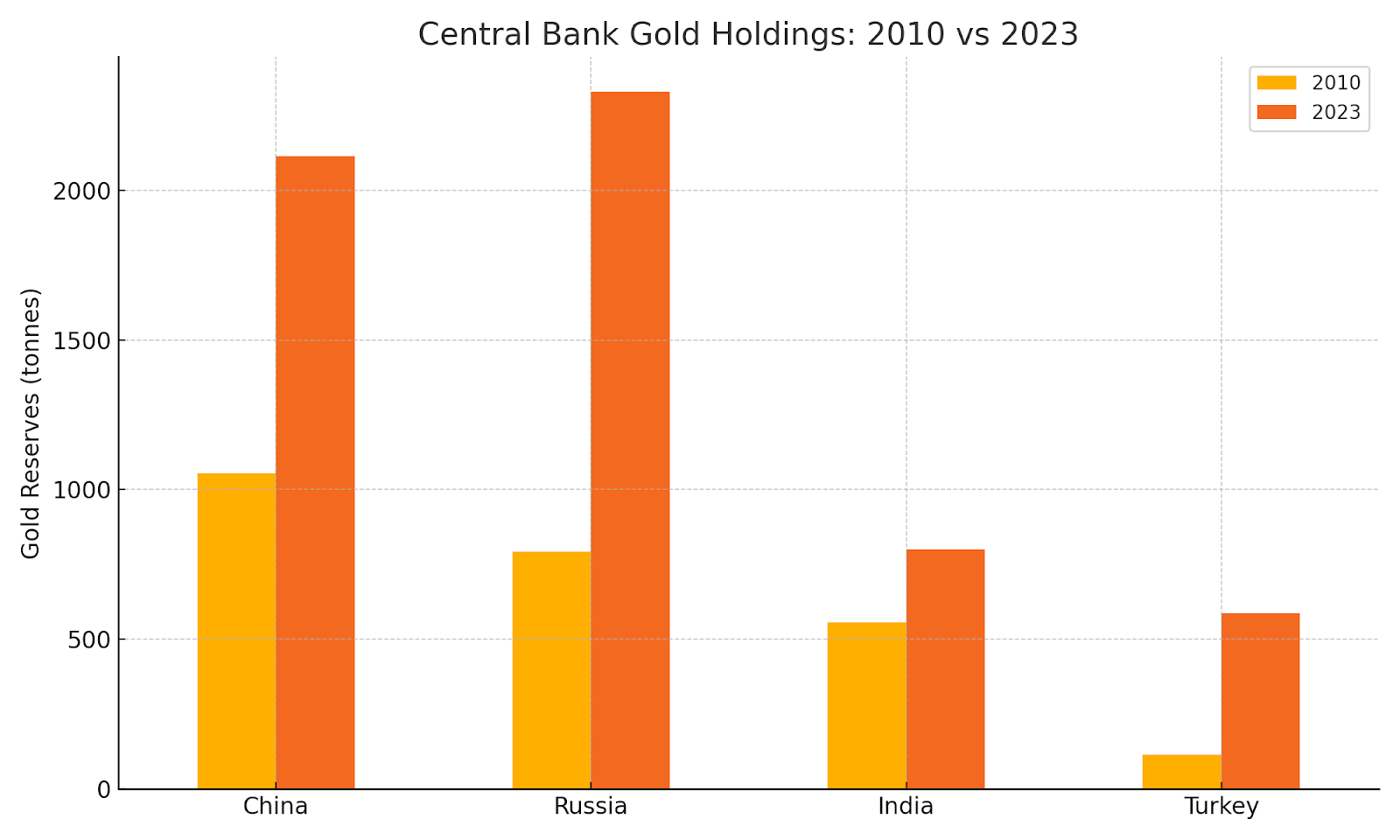

Figure 2: Central banks in emerging markets have increased their gold reserves significantly between 2010 and 2023.

Central bank demand has become increasingly influential in recent years. Many central banks—especially in emerging markets—have been diversifying away from the U.S. dollar by increasing their gold reserves. China, Russia, Turkey, and India have all substantially expanded their gold holdings, both to enhance financial security and to project economic sovereignty. When central banks become net buyers, as they have in recent years, the added demand supports higher prices.

Geopolitical tensions and war also drive gold prices higher, particularly when global conflict threatens major trade routes, disrupts economic stability, or stokes fears of broader escalation. Gold's role as a non-sovereign, apolitical store of value makes it uniquely suited to periods of global turmoil. Similarly, gold prices often respond sharply to major terrorist events, financial scandals, or shifts in global alliances.

Speculative trading via futures markets and ETFs (Exchange-Traded Funds) can amplify price movements. Gold is one of the most actively traded commodities on global exchanges such as COMEX and the London Bullion Market. Large institutional investors, hedge funds, and high-frequency traders can move the market quickly in response to technical signals, economic data releases, or momentum-based strategies. While this can create short-term volatility, it also increases liquidity and price discovery efficiency.

Environmental, Social, and Governance (ESG) standards are increasingly shaping the gold market. Ethical sourcing requirements by institutional investors, jewelry companies, and governments are putting pressure on gold producers to operate transparently and responsibly. This has led to higher compliance costs but also provides premium opportunities for miners who meet these standards. As sustainability becomes a priority for stakeholders across the supply chain, gold that is traceable and responsibly sourced may command higher prices in the global marketplace.

In conclusion, the price of gold is shaped by an array of intertwined forces: macroeconomic trends, interest rates, currency dynamics, central bank actions, geopolitical risks, speculative trading, and responsible mining practices. At iMARCK Resources, we use this deep understanding to structure deals, advise governments, and match investors with resilient and ethical gold opportunities. Our integrated view of the market helps our partners not only navigate volatility but capitalize on it—with clarity, confidence, and integrity.